David Carothers

CIC, CRM, CWCA

Principal of Florida Risk Partners. Founder of Killing Commercial. Host of The Power Producers Podcast. Author of The Extra 2 Minutes and The Dirty 130. Twenty-plus years in commercial risk.

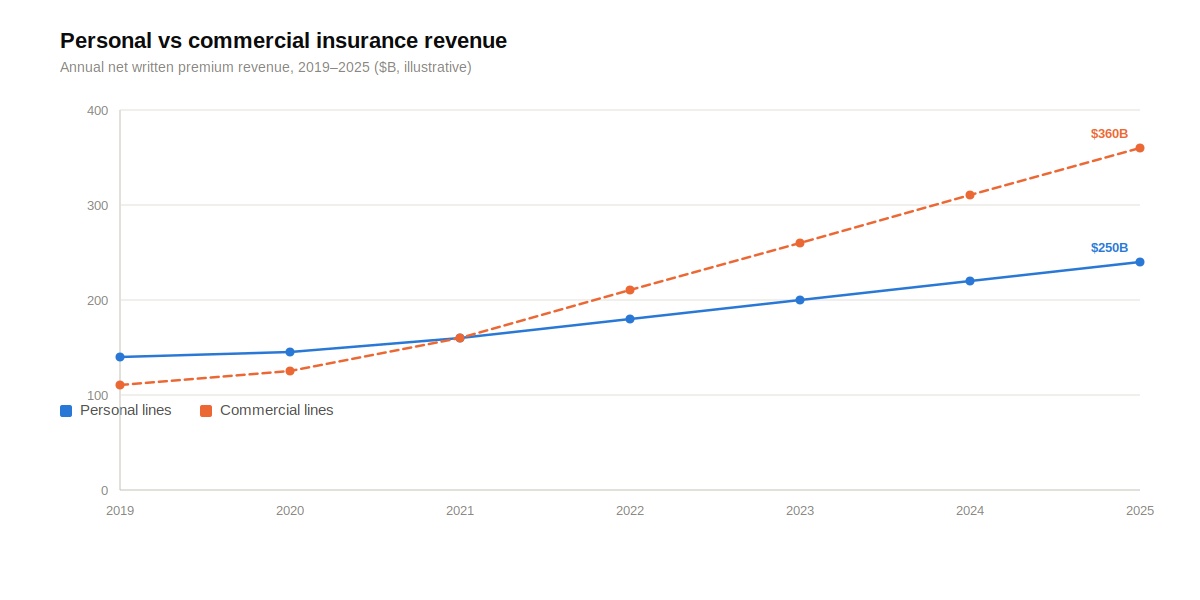

Commercial isn't one giant sale. It's 3× the premium per policy, on every policy, every line. Retention runs 90–95% vs. 85–90% for personal. The math compounds every year. The reason most personal-lines agencies write less commercial than they should is operational, not economic. We solve the operational problem.

The economics of commercial don't require chasing a single big mid-market deal. Whether you're writing a small BOP for a corner restaurant or a mid-market manufacturing account, commercial generates more revenue per producer hour invested than personal lines. The Insure AMS commercial build is the platform, structure, and automation that makes that math work — without building a new operational mess on top of the one you already have.

Higher premiums. Higher retention. More lines per account as the relationship matures. A commercial book doesn't just generate more revenue upfront — it generates more revenue on every renewal, with a client who adds coverage as their business grows. The agencies that move into commercial early build a book that compounds structurally. The platform removes the operational barriers that kept them out.

Commercial accounts have longer sales cycles, higher service requirements, and more moving parts at renewal. Personal-lines agencies that try to expand without the right platform end up with leads in spreadsheets, year-over-year re-quoting that happens when someone remembers, and COI requests falling through the cracks. The Insure AMS commercial build is the infrastructure that makes expansion feasible — not by adding headcount, but by giving the headcount you have the system to handle it.

You don't have to leap from personal lines to mid-market commercial. The Insure AMS small commercial playbook starts with BOPs, workers comp, and basic property — accounts your producers can write today. David Carothers and Kody Houk teach the sales side. We provide the platform underneath: the workflows, automation, and retention engine that make commercial production stick as your team's confidence grows.

Every commercial workflow built into HubSpot: lead qualification, multi-touch outreach, year-over-year re-quoting, policy-check workflow, service-ticket triage, audit prep, COI tracking. All on one timeline per account. No spreadsheets. No one-person-knows-how. The system holds the process so your team can run it.

Sales coaching from producers who've built commercial books, not consultants who've studied them. They trained the producers. They built the playbooks. We provide the platform underneath — so the coaching sticks because the system reinforces the process instead of fighting it.

Six core capabilities that run across every commercial account in your book, from the first lead touch to the renewal three years out.

Custom lead qualification, multi-touch outreach sequences, pipeline visibility by producer and by line. Year-over-year re-quoting activates dormant leads with zero incremental acquisition cost. Lost-quote recovery pipeline closes the loop on accounts that didn't close the first time.

Policy-check workflow, service-ticket triage by account tier, change tracking, and audit prep and support — all on one timeline per account. Complex commercial accounts stop slipping through the cracks when every touchpoint lives in one place.

Renewal intelligence briefings cut producer prep from hours to minutes. Real-time premium tracking shows the bleed as it happens. Automated outreach keeps every commercial account warm 90–120 days before renewal — whether you have 50 accounts or 500.

Certificate of insurance requests are among the highest-volume, lowest-value service tasks in commercial agencies. Insure AMS automates the request workflow and tracking so your CSRs handle exceptions, not the queue.

Lost commercial accounts don't stay lost. Win-back sequences run automatically on churned clients, timed to when competitor policies come up for renewal. Most commercial win-backs happen in year two or three — the platform makes sure you're there when the window opens.

Real-time premium tracking across your commercial book, by producer, by line, by account tier. Know where the revenue is, where it's growing, and where it's at risk — before the bleed becomes a problem, not after.

Bring your personal lines book, your current commercial volume, and your average commission per producer. We'll show you what one mid-market commercial account does to your P&L, and what the platform would cost to stand up versus what it pays back.